Why Waiting to Self-Direct Your IRA Gets More Expensive Every Year

Key Takeaways

Waiting to self-direct your IRA has a measurable cost in foregone compounding returns.

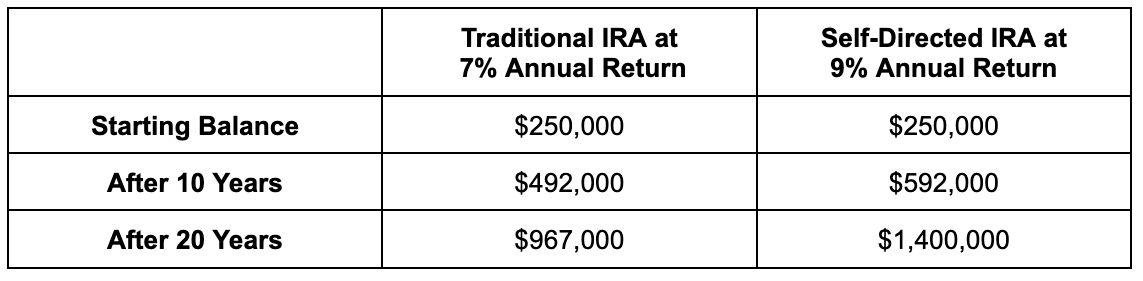

A $250,000 IRA generating 9% annual returns in alternative investments produces roughly $430,000 more over twenty years than the same balance earning 7% in a traditional account.

It's rarely too late to benefit from self-direction, but the cost of each additional year of waiting increases the longer you've already waited.

Waiting to self-direct your IRA feels like the responsible move. Or so that’s what we tell ourselves.

“I need to understand it better.”

“I’m waiting to find the right deal.”

“I’ll get on it once I have a bigger cash buffer.”

To a degree, these are reasonable, prudent positions. But the math treats waiting the same way, regardless of the reason for the delay.

Every year you wait, the compounding returns you lose snowball.

The Cost of Waiting Grows Every Year

A self-directed IRA (SDIRA) gives you access to alternative investments your IRA wouldn't otherwise allow, like real estate, private lending, private equity, and tax liens, whereas a traditional IRA limits you to stocks, bonds, and mutual funds.

Those alternative investments typically generate higher yields. Real estate held in an SDIRA can produce 6-10% cash-on-cash returns annually, and private lending commonly yields 8-12%. All of that income compounds inside a tax-advantaged account — tax-deferred in a traditional SDIRA, or entirely tax-free in a Roth.

That yield difference, compounded over time, is where we truly see the cost of waiting. Here’s an example:

The gap between accounts grows from $100,000 after ten years to more than $430,000 after twenty years. Those two percentage points of difference add up, and that’s the cost of waiting.

Every year you keep retirement funds solely in a traditional account while considering self-direction, you’re choosing a lower growth trajectory and creating a gap that gets harder and harder to close over time.

3 Reasons People Wait to Self-Direct Their IRA

In my experience, the hesitation almost always comes down to one of three things.

1. “I want to understand it better before I start.”

This is the most common reason people delay, and it’s also the one I have the most empathy for. Self-directed investing does have a learning curve. That said, it’s a lot steeper a curve in theory than in practice.

Investors who establish the structure first (even before identifying their first deal) learn faster because they’re evaluating real opportunities within a real framework. It’s hands-on, not theoretical.

If you wait until you feel fully prepared, you’ll wait forever because you’re chasing a moving target.

And I want to emphasize that the cost isn’t limited to foregone returns but extends to the deals you miss out on: private lending opportunities, real estate deals with short closing windows, syndications with limited availability — none wait for investors who aren’t ready to move.

2. “I’m waiting for the right deal.”

The right deal and the right structure are two very different things. You can’t act on the right deal if the account isn’t set up. Setting up a self-directed IRA doesn’t require you to invest right away; it just puts you in the position to move when something worth acting on appears.

3. “I need my balance to grow first.”

This one backfires in two ways. First, every month your balance grows inside a traditional IRA, it grows at a lower yield than it would in an SDIRA. If you're in a Roth, that also means every month of delay is a month of tax-free retirement investing you're leaving on the table.

Second, and more importantly, the IRA balance itself isn't the barrier: the structure is. Rolling over or transferring existing retirement funds into a self-directed account is straightforward. You don't need to accumulate more before you start, just redirect what you already have.

The Other Opportunity Costs

Beyond the math, there are other loss categories that you can’t see in a simple return comparison.

Roth conversion windows are one. Investors who convert traditional IRA funds to a Roth SDIRA during lower-income years (like a career transition, early retirement phase, or a year between positions) can lock in tax-free growth on everything that follows. Those windows close and cannot be easily replicated.

Estate planning is another. Assets that grow tax-free inside a Roth SDIRA can pass to heirs with significant tax advantages. The longer those assets have to compound tax-free, the greater the benefit. So a delayed start not only reduces your own retirement income, but also what you’re able to leave behind.

Finally, there are deal cycles. Real estate markets are always on the move, and private lending opportunities change with credit conditions. If you wait on the sidelines, you miss entire market windows, not just individual deals, and those conditions might not come back for a long time, if at all.

Is It Too Late to Redirect to a Self-Directed IRA?

It’s rarely too late. Investors in their 50s and 60s can still benefit meaningfully from self-direction. The strategy looks different with shorter time horizons, which favor income-generating assets over appreciation plays. Roth conversions will also require more careful tax planning. That said, the fundamental advantages of higher-yielding, tax-advantaged investing don't disappear with age.

What does change is the margin for error: a 45-year-old who waits five years to self-direct loses those five years but still has twenty ahead of them. A 60-year-old who waits five years loses a much larger share of their remaining compounding window.

All that said, the comparison above assumes consistent returns that no investment can guarantee. Success is not a foregone conclusion.

Alternative assets carry real risks, and the right balance between self-directed and traditional strategies depends on your individual situation, timeline, and risk tolerance. Most of the sophisticated investors I work with use SDIRAs alongside conventional accounts, not instead of them.

How Chicago Trust Administration Services Can Help

At Chicago Trust Administration Services, we work with investors who are ready to stop waiting by helping them get the right structure in place so they're prepared to act when the right opportunity arrives. Getting started doesn't require a deal in hand — it just requires a conversation.

To see how we can help, we invite you to schedule a complimentary meeting with us by calling 312-869-9394 or emailing steve@ctasira.com.

Frequently Asked Questions

Q: Can I move money from my existing traditional IRA into a self-directed IRA without paying taxes?

A: Yes. A direct rollover or trustee-to-trustee transfer from a traditional IRA to a self-directed IRA is not a taxable event. The funds move from one tax-advantaged account to another without triggering a distribution. The process is straightforward, and we handle the administrative steps with you at CTAS.

Q: Do I have to invest my entire IRA balance in alternative assets once I self-direct?

A: No. A self-directed IRA gives you the option to invest in alternative assets — it doesn't require you to do so with every dollar. Some investors self-direct a portion of their retirement funds while keeping the remainder in traditional investments. The key is having the structure in place so you can act on opportunities as they arise.

*The content and opinions in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

**CTAS professionals are not financial advisors and cannot provide advice or recommendations regarding specific investment decisions.