Is a Solo 401(k) the Smartest Self-Employed Retirement Plan for Independent Contractors?

Key Takeaways

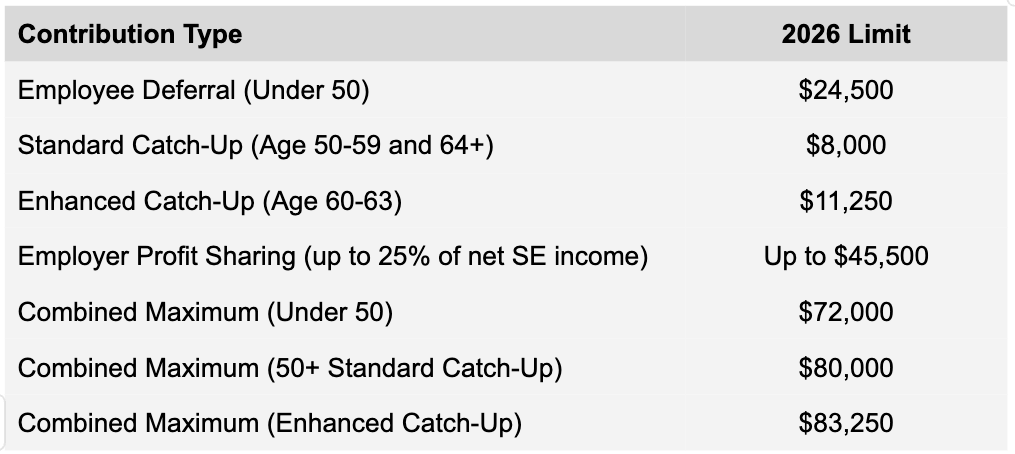

Independent contractors can contribute to a Solo 401(k) as both employee and employer, with combined limits up to $72,000 ($80,000+ with catch-up) in 2026.

Previous 401(k)s and traditional IRAs can be rolled into a Solo 401(k) as a direct, non-taxable transfer.

A self-directed Solo 401(k) can invest in real estate, private lending, private equity, and other alternatives, not just market-based securities.

A Self-Directed SEP IRA is a strong option for contractors seeking a simpler structure with meaningful contribution limits.

IRS compliance rules are strict; working with an experienced custodian protects the plan and the investor.

Most independent contractors I meet are sharp, disciplined, and financially savvy. To successfully build businesses, cultivate loyal client relationships, and control cash flow, you have to be. Still, when it comes to retirement planning, many of them wind up leaving significant opportunities on the table.

And some aren't planning at all — because they assume the right vehicle doesn't exist for them.

It does. The Solo 401(k) is one of the most powerful self-employed retirement plans available. And it doesn't have to sit in a brokerage account tracking the S&P 500. A self-directed Solo 401(k) can invest in real estate, private lending, private equity, and more — the same alternative assets that sophisticated investors have been using for decades.

What Is a Solo 401(k)?

Also called an Individual 401(k) or Self-Employed 401(k), a Solo 401(k) is a qualified retirement plan designed for self-employed individuals with no full-time employees other than a spouse. Consultants, freelancers, real estate professionals, and independent business owners all qualify.

What makes a Solo 401(k) different from a SEP IRA or SIMPLE IRA is the dual contribution structure. You contribute as both the employee and the employer — a distinction that matters enormously when you're deciding how much to set aside each year. It's also a genuine advantage over W-2 employees who are limited to employer-sponsored plans.

Here's the breakdown:

No other self-employed retirement plan comes close to this level of contribution flexibility.

Rolling Your Previous 401(k)s Into a Solo 401(k)

I often see contractors who survived corporate America, built up a solid 401(k), and then went independent. That old retirement plan is sitting at their former employer's brokerage, still invested in target-date funds, while they're now running their own operation.

All the while, they could roll previous 401(k) plans and traditional IRAs directly into a Solo 401(k) without triggering taxes or penalties. A direct rollover between custodians is a non-taxable event.

Consolidating your retirement assets into a single, self-directed structure gives you more capital to deploy into alternative investments and simplifies compliance tracking.

Your Solo 401(k) Isn’t Limited to Market Investments

Most independent contractors assume that a 401(k) means stocks, bonds, and mutual funds, and that assumption is costing them returns and diversification.

A self-directed Solo 401(k) can invest in the same alternative asset classes that sophisticated investors have been using for decades:

Real estate. Direct ownership of residential or commercial property, with income and appreciation growing tax-deferred inside the plan

Private lending. funding loans to real estate developers or businesses, earning 8–12% interest that compounds inside the plan

Private equity. Participating in growth-stage companies, syndications, or private placements.

Mortgage notes and tax lien certificates. Fixed-income alternatives backed by hard assets

In my experience, some of the best-positioned investors I work with are contractors who already understand real estate fundamentals from their professional work — engineers who've overseen construction, attorneys who've closed deals, consultants who advise commercial developers. And yet, they've kept their retirement savings in index funds.

When I ask why, the answer is almost always the same: "I didn't know I could do it."

All it takes is establishing a self-directed Solo 401(k) with a custodian who understands alternative investments — not a brokerage firm that processes only what's on their approved list. Your contributions flow into the plan, and the plan invests in the assets you identify, through compliant structures that your custodian helps you document properly.

What About a Self-Directed SEP IRA?

A Self-Directed SEP IRA is another strong option for independent contractors, particularly those who want a simpler setup and aren't focused on maximizing employee deferrals.

With a SEP IRA, you can contribute up to 25% of net self-employment income, with a 2026 maximum of $72,000. There are no employee deferrals and no catch-up contributions, but the administrative requirements are minimal.

For a contractor with relatively consistent income who isn't yet at the contribution ceiling, a Self-Directed SEP IRA can be an excellent entry point into alternative asset investing.

The key phrase in both cases is self-directed. Whether you go with a Solo 401(k) or a SEP IRA, the ability to invest beyond the stock market depends entirely on who holds your plan and whether they're equipped to facilitate alternative investments.

Compliance Is Never Optional

Don’t miss this: self-directed retirement plans carry compliance responsibilities that traditional brokerage accounts do not.

The IRS prohibits self-dealing, so your Solo 401(k) cannot invest in your own business, cannot transact with disqualified persons (you, your spouse, your children, your parents), and cannot benefit you personally before distribution.

If you violate these rules, even unintentionally, the consequences are severe. Your entire plan could lose its tax-advantaged status and become immediately taxable.

This is not a reason to avoid self-directed plans but a reason to work with a custodian who understands them.

How Chicago Trust Administration Services Can Help

At Chicago Trust Administration Services, we've spent more than two decades helping independent contractors, business owners, and sophisticated investors structure compliant self-directed plans. We open accounts in 7–14 days. We help you understand what's permitted before a deal is signed — not after.

If you're self-employed and ready to move beyond brokerage-based retirement accounts, let's have a conversation.

To see how we can help, we invite you to schedule a complimentary meeting with us by calling 312-869-9394 or emailing steve@ctasira.com.

Frequently Asked Questions (FAQs)

Q: Can I have a Solo 401(k) if I also have a part-time W-2 job?

A: Generally, as long as your self-employment business has no full-time employees, you can maintain a Solo 401(k) for that business. Contribution limits may be coordinated across plans. This is a nuanced area, so talk to your tax advisor and custodian before proceeding.

Q: What's the deadline to establish a Solo 401(k)?

A: For traditional Solo 401(k)s, the plan must be established by December 31 of the tax year in which you want to make contributions, though employee deferrals must be elected before year-end as well. Employer contributions can often be made up to your tax filing deadline, including extensions.

Q: Can I make Roth contributions to a Solo 401(k)?

A: Yes. Many Solo 401(k) plans allow Roth contribution designations on the employee deferral side. Roth contributions are made after-tax, but qualified distributions (including growth) are entirely tax-free.

*The content and opinions in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

**CTAS professionals are not financial advisors and cannot provide advice or recommendations regarding specific investment decisions.