Consultants and Firm Owners: The Solo 401(k) Advantage for Alternative Investments

Key Takeaways

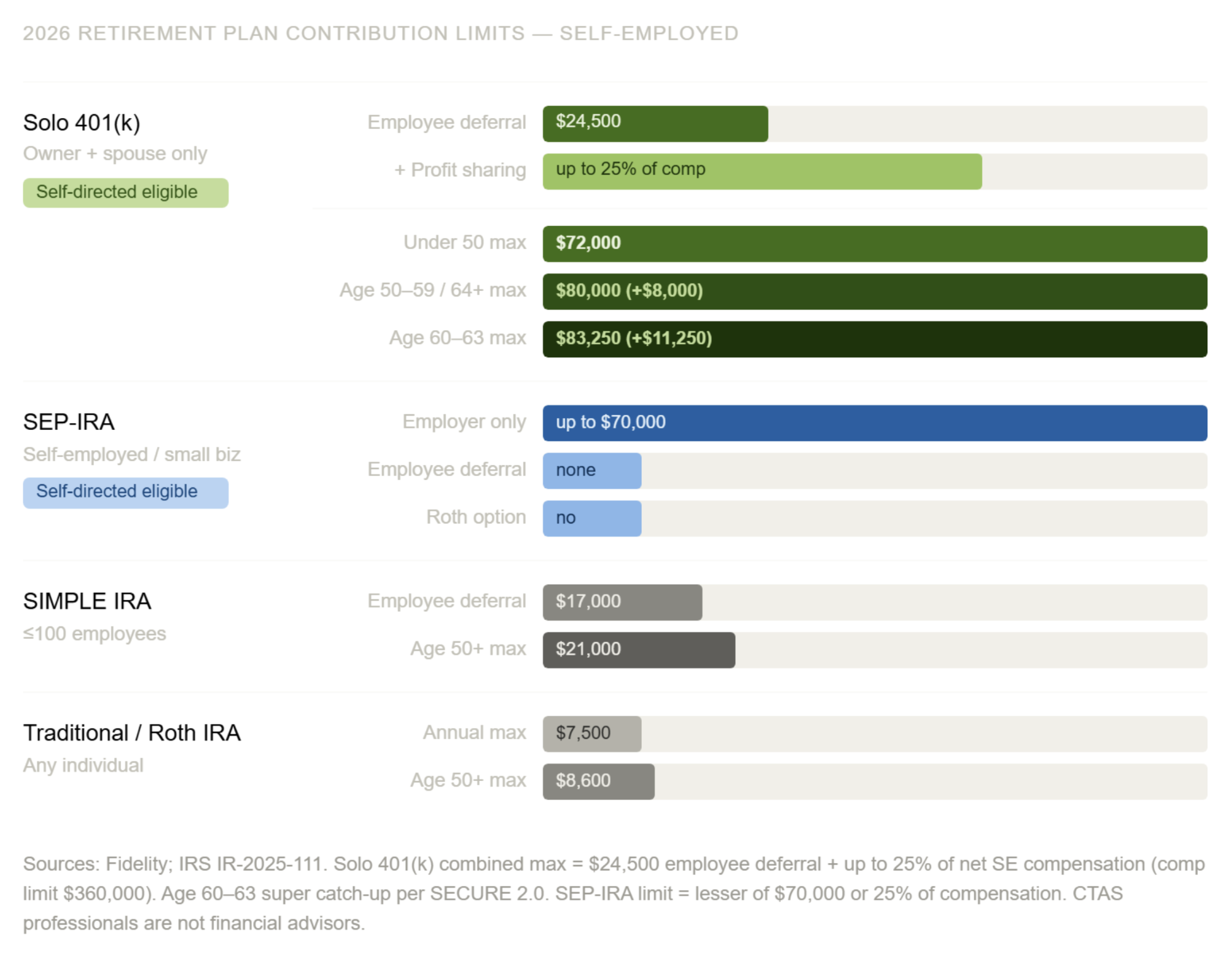

For 2026, solo 401(k) contribution limits allow up to $72,000 per participant under age 50, far exceeding the limit for a traditional IRA.

A self-directed 401(k) plan lets consultants and firm owners invest in real estate, private lending, private equity, and other alternative assets that institutional plans restrict.

The dual contribution structure of a solo 401(k), employee deferrals plus employer profit-sharing, can be used strategically to fund alternative investments in the same year income is earned.

Compliance rules governing self-directed 401(k)s are strict. Prohibited transactions, disqualified persons, and plan document requirements must all be managed carefully from the start.

Consultants and firm owners who come to me about self-directed investing often face the same problem. After years of building expertise in their industries, they want to put that knowledge to work in their retirement accounts.

But most of them are sitting with SEP-IRAs or SIMPLE IRAs, which both limit their annual contributions and offer no path to alternative assets.

The solution is in the solo 401(k).

When structured correctly, this plan type offers higher contribution ceilings, more investment flexibility, and compliance protections that most institutional plans can’t provide.

For consultants and firm owners with variable income and strong deal flow, it can be one of the most efficient retirement vehicles available.

What Makes a Self-Directed 401(k) Plan Different?

A standard 401(k) offered through a major brokerage limits you to mutual funds, ETFs, and target-date funds. A self-directed 401(k) plan (sometimes called a solo 401(k) or individual 401(k) when structured for owner-only businesses) operates under the same IRS framework but gives you control over which assets the plan holds.

So your plan can invest in residential and commercial real estate, private lending, mortgage notes, tax liens, private equity, and other alternative asset classes. The income those investments generate flows back into the plan, where it grows tax-deferred.

The key distinction between a self-directed 401(k) and a self-directed IRA is contribution limits.

With an IRA (even a SEP-IRA), your annual contribution ceiling is lower and comes from a single source. A solo 401(k) uses a dual structure.

Solo 401(k) Contribution Limits for 2026

The gap between a solo 401(k) and every other self-employed plan option widens further depending on your age. The dual contribution structure drives it: employee deferral plus employer profit-sharing, both in the same year.

For consultants and firm owners with strong earning years, that gap directly translates into how quickly you can build a meaningful pool for alternative investments.

How Consultants Typically Use This Structure

The self-employed professionals I work with most often use their self-directed 401(k) plans in a few specific ways.

Private lending is the most common. A consultant or firm owner with real estate expertise can fund short-term bridge loans or acquisition financing through their plan. The borrower pays interest directly into the 401(k), where it compounds tax-deferred. Rates on these often range from 8% to 12%, which is above what most fixed-income alternatives offer.

Real estate direct ownership is another. If you have experience evaluating commercial properties, multifamily buildings, or industrial assets, you can purchase them inside your plan. Rental income flows back into it. When the property appreciates and is sold, the gain remains within the tax-deferred structure.

Private equity and startup investments also work well for professionals who have built networks within their specific industries. Subscription agreements, PPMs, and convertible notes can all be held inside a properly structured self-directed 401(k) plan.

Recently, I’ve seen consultants in technology-adjacent industries accelerate their deal flow to fund early-stage companies. AI is reshaping how these firms are valued and how quickly they move, creating both opportunities and due diligence pressure for investors who haven’t kept pace with how quickly these businesses evolve.

Compliance Rules to Follow Diligently

A self-directed 401(k) plan is subject to the same prohibited transaction rules as any qualified retirement plan. Violations are severe. The IRS can disqualify the entire plan, making its full value immediately taxable.

The core rules:

Your plan cannot transact with disqualified persons. That includes you, your spouse, your lineal descendants, and certain business entities you control. You cannot sell an asset you personally own to your plan, nor can you buy from it.

You cannot receive personal benefit from plan-owned assets. If your 401(k) owns a rental property, you cannot use it personally — not for a weekend, not at any time.

All income and expenses flow through the plan. No commingling with personal or business accounts.

The plan document itself must be properly drafted and maintained. A solo 401(k) that was set up years ago and never updated may not permit alternative investments at all.

I've seen investors move forward on a deal only to find their plan document restricted them from the asset class they intended to purchase. That kind of discovery mid-transaction is costly but completely avoidable.

What Chicago Trust Administration Services Does Differently

Most large custodians are set up to handle stocks and mutual funds. When you bring them a private lending deal or a real estate LLC interest, the process slows considerably, and in some cases, they'll decline to hold the asset at all.

At Chicago Trust Administration Services, alternative investments are what we do. We understand the asset classes, the regulatory framework, and the documentation requirements. We open accounts and fund investments in 7 to 14 days, which is the timeline you need when you're working with deal partners who have capital call deadlines.

If you're a consultant or firm owner evaluating whether a self-directed 401(k) plan makes sense for your situation, the conversation starts with understanding what you want to invest in, what your income structure looks like, and whether your current plan documents give you the flexibility you need.

To see how we can help, we invite you to schedule a complimentary meeting with us by calling 312-869-9394 or emailing steve@ctasira.com.

Frequently Asked Questions

Q: Can I have both a solo 401(k) and a SEP-IRA at the same time?

A: Generally, yes — but contribution limits interact, and having both plans complicates your annual calculations. The IRS applies a single combined limit across employer contributions regardless of how many plans you participate in. Before maintaining both simultaneously, this should be reviewed with a tax professional familiar with self-employed retirement plans.

Q: What happens to my self-directed 401(k) if I hire employees?

A: A solo 401(k) is only available to businesses with no full-time employees other than the owner and a spouse. If you hire eligible full-time staff, the plan must be converted to a traditional 401(k) with all the participation and nondiscrimination requirements that entail. This is one of the most common structural issues I see when a consultant's business grows.

Q: Can I make Roth contributions to a solo 401(k)?

A: Yes, if your plan document includes a Roth provision. Roth solo 401(k) contributions are made after-tax, but qualified distributions — including all the growth from alternative investments — come out tax-free.

*The content and opinions in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

**CTAS professionals are not financial advisors and cannot provide advice or recommendations regarding specific investment decisions.